The secondary bond market began the week on a positive note, witnessing robust transaction volumes and a continued decline in yields on May 6, 2024. Trading activity primarily focused on the short to medium end of the yield curve, particularly on tenors ranging from 2026 to 2032. Notably, the 15.12.26 maturity attracted significant interest, with yields dropping to an intraday low of 10.63% from a high of 10.70%, supported by strong trading volumes. Similarly, other 2026 tenors experienced yield declines, with the 15.05.26 and 01.06.26 tenors falling from an intraday high of 10.60% to a low of 10.50%.

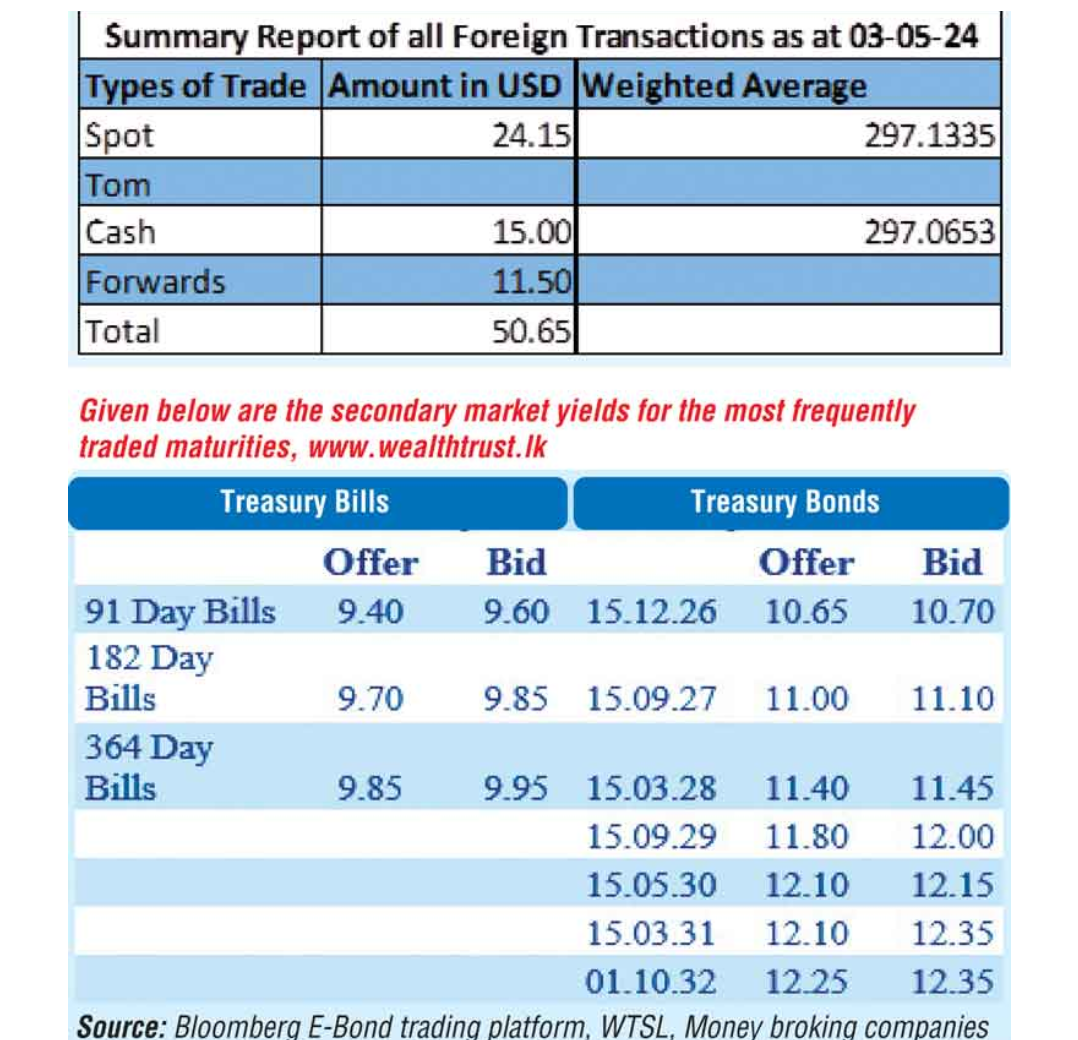

Moreover, the 2028 tenors, including 15.03.28, 01.05.28, and 01.07.28, saw yields dip to intraday lows of 11.40% from highs of 11.58%. Trades were also observed on the 2027 tenors, hitting intraday lows of 10.95% from highs of 11.05%. Additionally, transactions occurred on longer tenor bonds, such as 15.05.30 and 01.10.32, at rates ranging from 12.10% to 12.35%. The total secondary market Treasury bond/bill transacted volume for May 3 amounted to Rs. 21.21 billion. In money markets, the weighted average rates for overnight call money and repo stood at 8.64% and 9.14%, respectively.

Furthermore, the net liquidity surplus stood at Rs. 139.25 billion, with the Central Bank withdrawing Rs. 9.00 billion from the SLFR and receiving deposits of Rs. 188.25 billion at the SDFR. The Central Bank injected liquidity through overnight and 7-day term reverse repo auctions for Rs. 10.00 billion and Rs. 30.00 billion, respectively, at weighted average rates of 8.65% and 8.85%. In the Forex market, the USD/LKR rate on spot contracts closed the day at Rs. 298.00/298.50, depreciating from the previous day’s closing level of Rs. 297.15/297.35. The total USD/LKR traded volume for May 3 was $50.65 million.