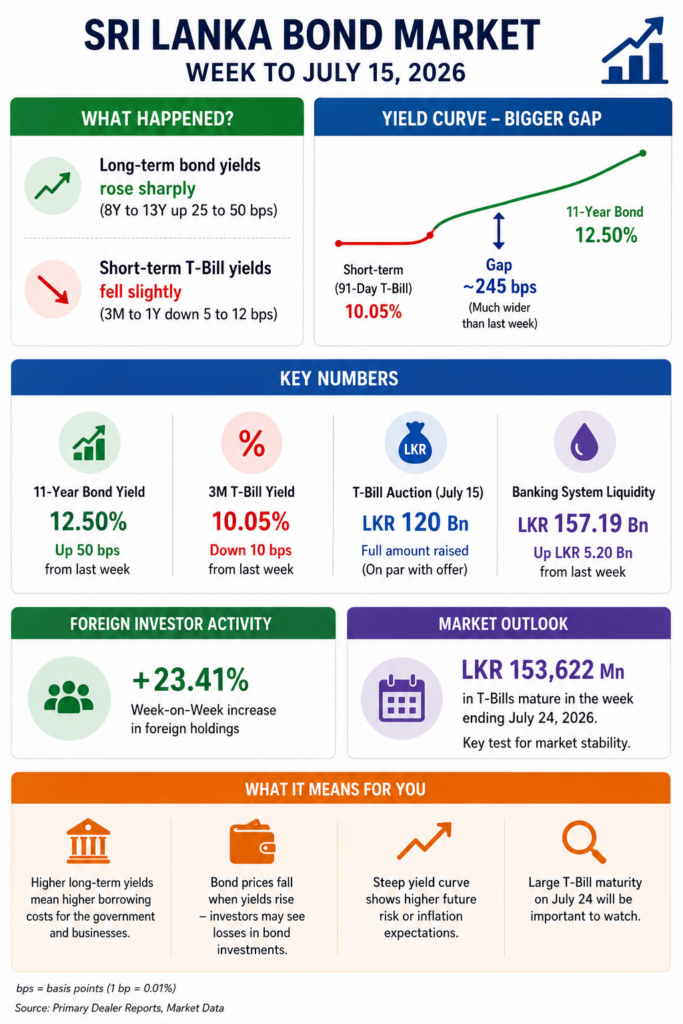

Medium and long-tenor government bond yields recorded their largest weekly increases of the year in the week to July 15, while short-end T-Bill yields moved in the opposite direction, producing a pronounced steepening of the yield curve.

Sri Lanka’s secondary bond market recorded a sharp rise in medium and long-tenor yields in the week to July 15, 2026, with the 11-year tenor posting the largest increase at 50 basis points and the 13-year tenor rising 48 basis points compared to the prior week. The scale and breadth of the moves represent the most significant weekly yield shift recorded in the secondary market across the reporting period tracked since late June.

The increases were concentrated in the middle and longer segments of the curve. The 9-year tenor rose 30 basis points to 12.15%, while the 8-year and 10-year tenors each gained 25 basis points to 12.00% and 12.20% respectively. The 6-year and 7-year tenors each rose 15 basis points to 11.75% and 11.85%, while the 4-year tenor gained 15 basis points to 11.45% and the 5-year tenor rose 20 basis points to 11.60%. The 2-year tenor edged up 5 basis points to 10.75%, while the 3-year held unchanged at 10.95%.

The direction at the short end of the curve was the opposite. Secondary market yields on the 3-month, 6-month and 1-year T-Bill tenors declined 10, 5 and 12 basis points respectively to 10.05%, 10.20% and 10.15%. The weekly T-Bill auction conducted on July 15 confirmed this short-end easing, with the weighted average yield on the 91-day bill falling 8 basis points to 10.13%, the 184-day bill declining 3 basis points to 10.27% and the 364-day bill easing 1 basis point to 10.20%. The PDMO raised the full offered amount of LKR 120.0 billion at the auction, with LKR 55.0 billion accepted at the 91-day tenor, LKR 35.0 billion at the 184-day tenor and LKR 30.0 billion at the 364-day tenor.

The simultaneous decline in short-end yields and surge in longer-dated yields constitutes a pronounced steepening of the yield curve. The spread between the 91-day T-Bill secondary yield at 10.05% and the 11-year bond at 12.50% now stands at approximately 245 basis points, a materially wider gap than what prevailed just one week earlier. A steepening yield curve of this nature typically reflects market expectations of higher rates or elevated risk premium at longer durations, even as near-term liquidity conditions remain accommodative.

Secondary market trading on July 15 was subdued, with activity concentrated in the 2030 segment. The 15.03.2030 maturity traded at 11.33%, while the 01.07.2030 and 01.08.2030 maturities both changed hands at 11.50%. The 15.10.2030 bond traded at 11.60%, broadly unchanged from prior session levels. Further along the curve, the 01.11.2033 maturity traded at 11.95%, while the 15.06.2034 and 15.10.2034 bonds both settled at 12.10%. At the long end, the 01.07.2037 maturity was seen trading at 12.65%.

The July 13 Treasury Bond auction provided additional reference points for longer-dated pricing. Phase 2 results confirmed a weighted average yield of 11.97% for the 11.00%/2030 ‘B’ tenor, 12.04% for the 11.70%/2034 ‘W’ tenor and 12.58% for the 10.75%/2037 ‘W’ tenor, with total Phase 2 bids of LKR 15,155 million. The 2037 tenor settling at 12.58% at auction is consistent with secondary market pricing at the long end and reinforces the upward shift in longer-duration yield expectations.

Foreign holdings of government securities rose 23.41% week-on-week, a sharp increase in international participation in the local bond market. Total outstanding government securities stood at LKR 18,515.48 million as of July 15, a marginal week-on-week increase of 0.04%, comprising LKR 16,136 million in Treasury Bonds and LKR 2,380 million in Treasury Bills.

Banking system excess liquidity expanded to LKR 157.19 billion from LKR 151.99 billion in the prior session, continuing the elevated liquidity environment that has characterized the market since early July. The combination of record-high system liquidity and sharply rising longer-dated yields suggests that the liquidity surplus is not translating into increased demand at the longer end of the curve, where investors are demanding higher yields to extend duration.

A significant maturity event is approaching in the week ending July 24, when LKR 153,622 million in T-Bills falls due for settlement. How the market absorbs this maturity alongside prevailing yield pressures at the longer end will be a critical test of near-term fixed income conditions.

Key Numbers:

| Tenor | July 15 Yield | July 8 Yield | Weekly Change |

|---|---|---|---|

| 3M T-Bill (Secondary) | 10.05% | 10.15% | -10 bps |

| 6M T-Bill (Secondary) | 10.20% | 10.25% | -5 bps |

| 1Y T-Bill (Secondary) | 10.15% | 10.28% | -12 bps |

| 2Y | 10.75% | 10.70% | +5 bps |

| 4Y | 11.45% | 11.30% | +15 bps |

| 5Y | 11.60% | 11.40% | +20 bps |

| 8Y | 12.00% | 11.75% | +25 bps |

| 9Y | 12.15% | 11.85% | +30 bps |

| 10Y | 12.20% | 11.95% | +25 bps |

| 11Y | 12.50% | 12.00% | +50 bps |

| 13Y | 12.60% | 12.13% | +48 bps |

| 91-Day T-Bill Auction | 10.13% | 10.21% | -8 bps |

| 184-Day T-Bill Auction | 10.27% | 10.30% | -3 bps |

| 364-Day T-Bill Auction | 10.20% | — | -1 bp |

| T-Bill Amount Raised | LKR 120.0 Bn | — | On par with offer |

| Banking System Liquidity | LKR 157.19 Bn | LKR 151.99 Bn | +LKR 5.20 Bn |

Business Impact:

A 50 basis point weekly rise in the 11-year tenor and near-equivalent moves across the 8-year to 13-year segment represents a material repricing of long-duration risk in the Sri Lankan bond market. For the government, higher long-term yields increase the cost of servicing existing debt and raise the benchmark against which new long-term borrowing is priced. For businesses planning long-term financing, the sharp rise in longer-dated yields means that fixed-rate borrowing costs have moved significantly higher in a short period. Companies with existing fixed-income portfolios will face mark-to-market losses as bond prices fall in response to rising yields. The steepening of the yield curve is a signal that fixed income investors are pricing in either higher inflation expectations, increased duration risk or a combination of both at the longer end, even as near-term liquidity remains ample and short-end rates ease. CFOs and treasury teams with long-term financing decisions pending should factor this repricing into their cost-of-capital assumptions. The LKR 153,622 million T-Bill maturity due in the week ending July 24 will be the next major market event to watch, as reinvestment decisions at that scale could influence both short and medium-term yield dynamics.

Source Attribution:

Source: Central Bank of Sri Lanka statistics and publicly available fixed income market information.