Govt. cash surplus due to overborrowing, says Verité, highlighting that Sri Lanka’s improved Treasury liquidity may mask underlying fiscal pressures driven by excess borrowing and rising interest costs.

Govt. cash surplus due to overborrowing, says Verité despite stronger liquidity

Govt. cash surplus due to overborrowing, says Verité, as Sri Lanka’s Treasury cash position has shifted dramatically from a deficit of 832 billion rupees in 2022 to a surplus exceeding 1.2 trillion rupees by August 2025. According to Verité Research, this apparent improvement in liquidity does not necessarily indicate a stronger fiscal position, but rather reflects a buildup of borrowed funds held as cash.

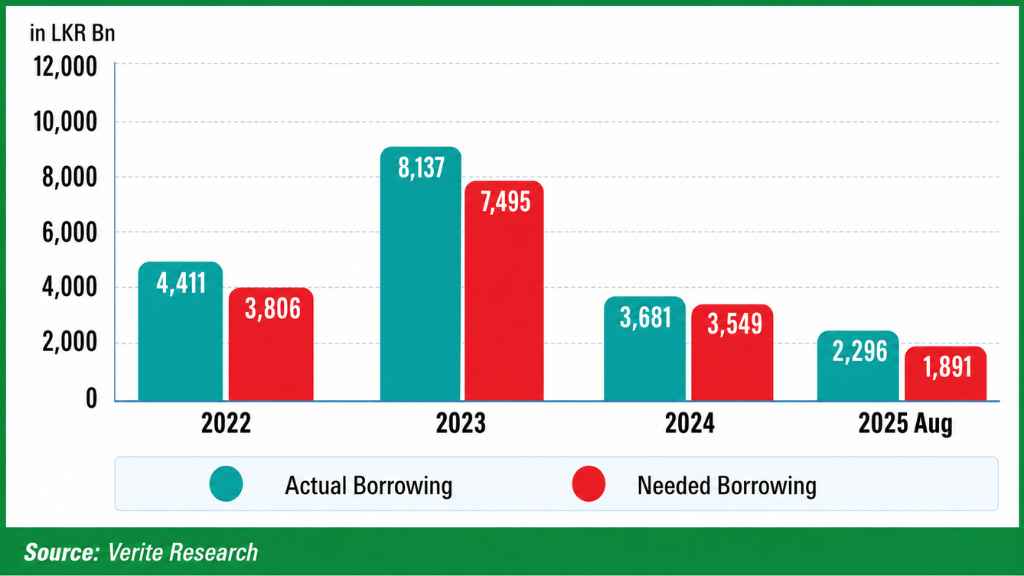

The think tank noted that the increase in cash balances was driven by borrowing beyond immediate financing needs. Between 2022 and August 2025, the government borrowed approximately 1.78 trillion rupees more than required to cover budget deficits and debt repayments. Instead of being used to reduce outstanding liabilities, these funds were retained as a cash buffer in the Treasury.

Govt. cash surplus due to overborrowing, says Verité, emphasizing that this dynamic can create a misleading perception of fiscal strength. While a rising cash balance may suggest improved financial health, it is effectively offset by a corresponding increase in debt. Analysts explain that this situation is similar to taking out a loan and holding the proceeds in a bank account—cash levels rise, but liabilities increase by the same amount, leaving net financial position unchanged.

Data from the Ministry of Finance Sri Lanka indicates that the pattern was particularly evident in 2023. During that year, the government’s total financing requirement stood at 7,495 billion rupees, including 5,331 billion rupees in debt repayments and a budget deficit of 2,164 billion rupees. However, total borrowing reached 8,137 billion rupees, resulting in an excess of around 642 billion rupees that was added to the Treasury’s cash reserves.

Govt. cash surplus due to overborrowing, says Verité, pointing out that while such a cash buffer improves short-term liquidity, it also carries significant costs. The government must pay interest on the borrowed funds, while the returns earned on cash balances are typically lower. This mismatch results in a net financial loss over time, increasing the overall interest burden on public finances.

The analysis highlights a key trade-off. On one hand, higher cash reserves provide flexibility, allowing the Treasury to meet urgent financing needs without resorting to immediate borrowing. This can be particularly useful in managing bond auctions, where the government may choose to delay borrowing if market yields are deemed too high. On the other hand, maintaining excessive cash balances leads to higher debt servicing costs, which can weigh on long-term fiscal sustainability.

Govt. cash surplus due to overborrowing, says Verité, cautioning that an overbuilt cash buffer can ultimately weaken the fiscal outlook. While liquidity improves, the underlying fiscal position may deteriorate due to the additional interest burden associated with unused funds. The think tank stressed that a balanced approach is necessary, where cash reserves are maintained at optimal levels without incurring unnecessary costs.

Despite these concerns, recent fiscal data shows significant progress in Sri Lanka’s budget performance. In January 2026, the government recorded a sharp improvement, with the primary surplus rising by 86.7 percent year-on-year to 222.82 billion rupees. The overall budget deficit narrowed by 96.8 percent to just 3.81 billion rupees, indicating a near-balanced fiscal position.

Revenue growth has been a key driver of this improvement, supported by stronger tax collections. Government income increased by over 35 percent, while expenditure growth remained contained at around 1.4 percent. This combination of rising revenues and controlled spending has contributed to ongoing fiscal consolidation efforts.

The improved fiscal position has also created space for targeted policy measures. Authorities have introduced a 100 billion rupee short-term relief package aimed at cushioning the impact of global energy shocks, while continuing to manage post-disaster spending requirements.

However, Verité Research maintains that these gains should be viewed in context. While fiscal consolidation is evident, the accumulation of excess cash through borrowing raises questions about the efficiency of debt management strategies. Ensuring that borrowed funds are used productively, rather than held idle, will be critical to strengthening the overall fiscal framework.

Looking ahead, policymakers face the challenge of balancing liquidity management with debt sustainability. Maintaining adequate cash reserves is important for financial stability, but excessive accumulation can lead to unnecessary costs and distort fiscal indicators.

Govt. cash surplus due to overborrowing, says Verité ultimately underscores the complexity of assessing fiscal health. While headline indicators such as cash balances may show improvement, a deeper analysis reveals the underlying trade-offs between liquidity, debt, and long-term sustainability in Sri Lanka’s public finances.